When buying a home, many homebuyers tend to search for the best mortgage interest rates available. While some may find that perfect rate, others may opt to take advantage of lender-provided options, such as mortgage points.

Mortgage points are designed to help buyers bring down their interest rates by paying them ahead of time. Sometimes considered “discount points,” mortgage points allow you to pay a larger down payment up front to quell your interest rates throughout the life of your loan.

While that sounds like an excellent option for those searching to put a dent in their future monthly payments, there are a few items to consider.

Here are some pros and cons of mortgage points and tips on what to do for your situation:

Mortgage point pros

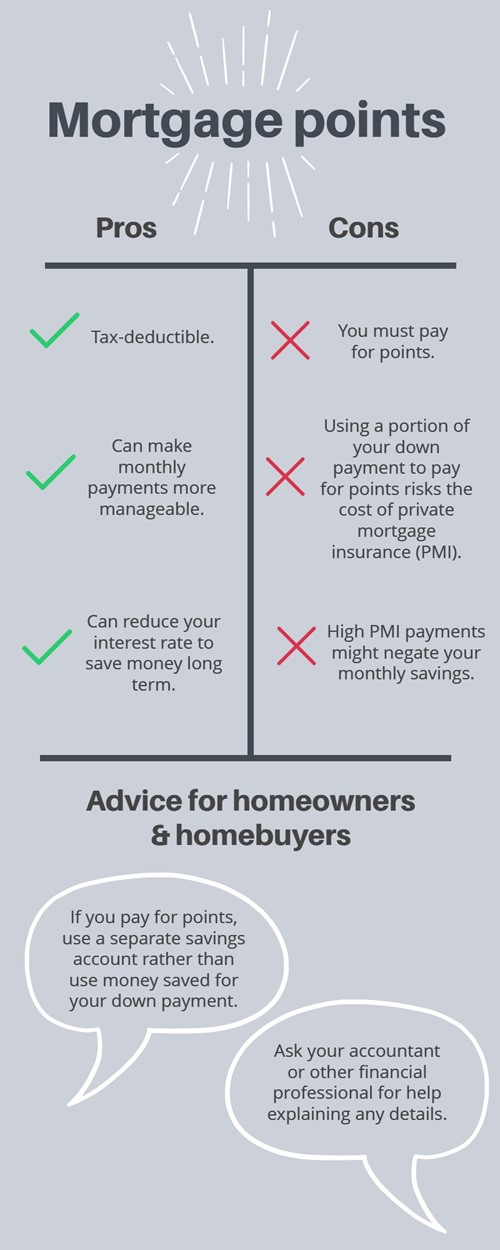

When delving into the world of mortgage discount points, the immediate hook is your monthly savings in the long term. Mortgage points are exceptional ways to bring your mortgage interest rate into a desirable range, creating more manageable payments on a monthly basis.

Another fantastic feature of mortgage points is they’re tax-deductible. According to the IRS, you can itemize your deductions on a Schedule A, or Form 1040, and only need to meet a few requirements, such as using the “cash method” for tax reporting. You’ll also need to have your primary residence as the loan’s security method.

Mortgage point cons

There are great advantages to discount points. However, there are a few cons that may surface with this kind of lender program. For example, if you plan to pay for mortgage points, try to secure a secondary savings account to make that payment instead of taking it from your down payment.

If you take the funds from your initial down payment, you could end up paying less than the 20% needed to avoid private mortgage insurance, or PMI. Since PMI can increase your monthly payments, you may end up paying more on your monthly mortgage than you’d save, or you could end up pushing out your break-even point, prolonging your larger payments.

Homeowner and homebuyer advice

There are ways to use mortgage points to your advantage. For starters, make sure you have an in-depth understanding of your current monthly finances, your projected finances and a financial roadmap for the next few years that you can follow easily.

Another fantastic idea is to get in touch with your loan officer or lender. Have them explain your options, what the estimates are for the next few years (or further) and any tips they may have for you. If you find yourself in the beginning stages of your home search, ask your real estate agent for any connections or recommendations to a lender or loan officer.

About the Author

Taylor Stewart

Taylor Stewart was born and raised in Richmond, Va. He attended Elon University on a baseball scholarship, but after suffering an unlikely injury, he was forced to give up on his dreams of making it to the big leagues.In 2006, Taylor moved to Bonita Springs, FL to pursue a career as a Professional Golfer. After traveling up and down the east coast of the United States playing in various golf tournaments on various golf tours, Taylor suffered yet another injury and was forced to change his career plans. Now, as a real estate agent,Taylor as chosen to put the same drive and determination that made him successful in sports, into helping others find their own piece of paradise in southwest Florida. Especially for those living in or looking for that perfect golf community, Taylor is able to guide his buyers and sellers through his expertise of the golf game and southwest Florida golf courses. Taylor is"Your ace in the hole."